The Conversation

The Conversation

Mortgage fraud is back in the news. Lisa Cook, a Federal Reserve governor, is being investigated by the Department of Justice for allegedly making false statements when applying for a mortgage. Members of Donald Trump’s Cabinet are accused of similar wrongdoings. Could any of these people go to prison?

Mortgage fraud is not a new problem. Subprime mortgage fraud fueled the 2008 financial meltdown, when large numbers of very risky mortgages defaulted. Mortgage fraud was also a key feature of the savings and loan crisis in the 1980s.

Mortgage applications are very long, so there’s plenty of opportunity to make mistakes. Plus, they require borrowers to declare that everything is “true, accurate, and complete.” Misrepresentation can trigger potentially large civil and criminal penalties.

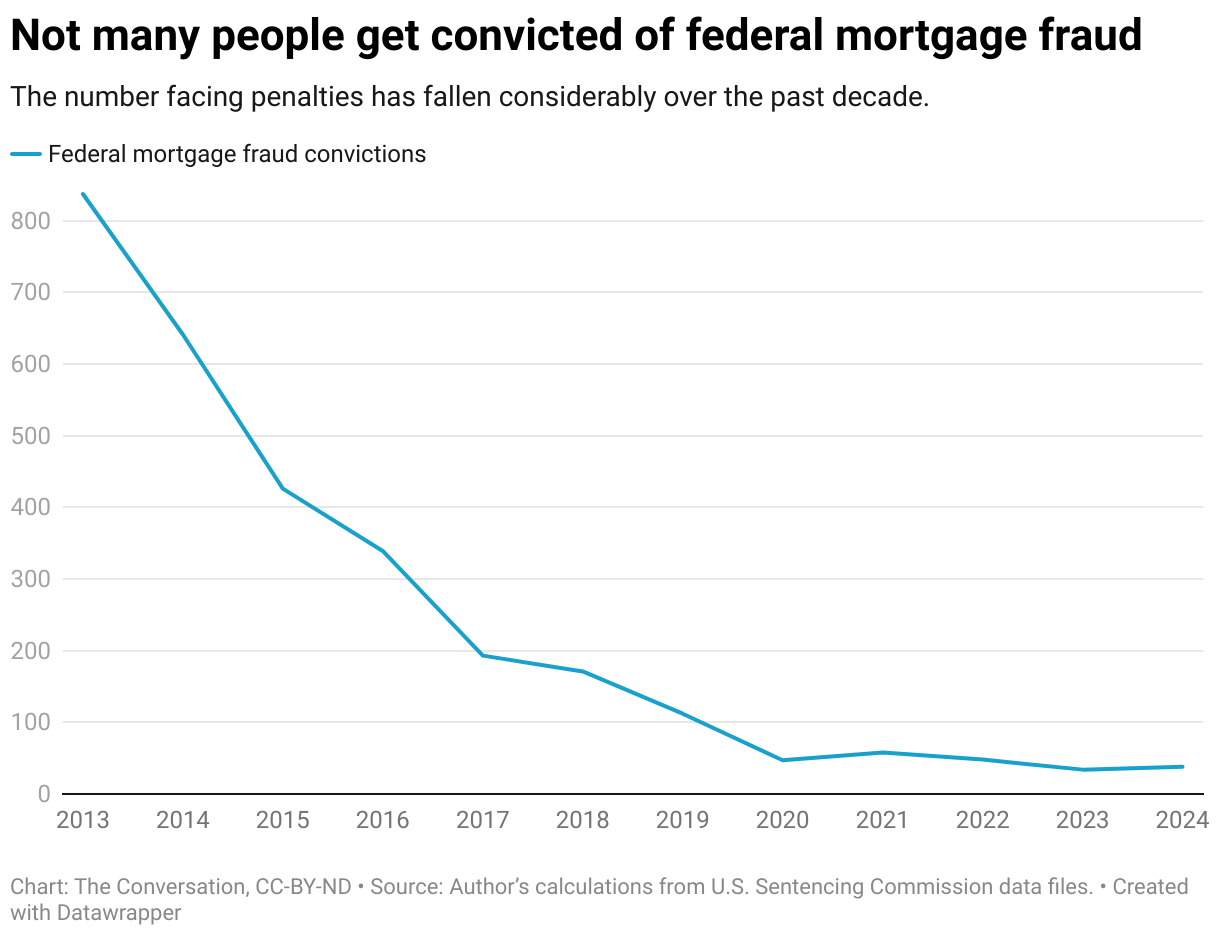

As a business school professor, I was curious how many people are convicted of mortgage fraud today. After all, relatively few people went to jail for fraudulent loans back in 2008. Since most mortgage fraud violates federal law, I looked at more than a decade of federal conviction data. What I found was clear: Almost no one has gone to federal prison recently for lying on a mortgage application.

What is mortgage fraud?

Mortgage fraud is when someone intentionally misrepresents facts in order to obtain a property loan. People can lie about many things on a mortgage application, such as their income, assets or employment status, or whether they will occupy the home being purchased or rent it out.

Being caught lying to get a mortgage can be costly. The maximum federal sentence is 30 years, with fines of up to US$1 million. Because more than a quarter of all mortgages are guaranteed by federal agencies, and many are acquired by quasi-government organizations like Freddie Mac and Fannie Mae, most mortgage fraud is a federal crime.

However, just because there are laws on the books doesn’t mean they’re enforced. For example, I work in Boston, where for years jaywalking has been illegal – but as any visitor quickly notices, no one pays any attention to this rule.

How many people are convicted?

The U.S. Sentencing Commission provides detailed data on every person convicted of federal crimes since 2013. The database is large, since federal courts convict almost 70,000 people each year.

However, very few people are convicted of federal mortgage fraud. Just 38 people in the country were sentenced for such crimes in 2024, and among that small group, four of the convicted got no prison time. A year earlier, just 34 people were convicted and seven avoided prison.

Over the past dozen years, fewer than 3,000 people were convicted of federal mortgage fraud, and the number of people sentenced fell steadily each year.

Three thousand people are a tiny fraction of mortgages issued. The Consumer Financial Protection Bureau estimates that almost 100 million new mortgage loans were written to purchase or refinance a home over the past 12 years. For those who like precision, 3,000 is only 0.003%.

The Sentencing Commission’s files also offer insight into who gets convicted of mortgage fraud. Three-quarters were men. More than 90% were U.S. citizens. The typical person convicted of mortgage fraud is a man in his late 40s with an associate degree, the data suggests.

The real penalty

While the maximum penalty is 30 years, almost no one serves that long a sentence. In 2024, the maximum sentence handed out was just 10 years. Since 2013, 15% of those convicted got no jail time. The average sentence for people who did get jail time was 21 months, which is less than two years behind bars.

Fines are also much lighter in practice than the maximum $1 million penalty. In 2024, the maximum fine passed down was a quarter-million dollars. Since 2013, the average person convicted of mortgage fraud paid a fine of less than $6,000, with over half of all those convicted paying no fine at all.

Now not paying a fine or only paying a small one doesn’t mean there’s no financial penalty. The courts required most of those convicted to make restitution. In 2024, half of all people convicted had to pay at least a half-million dollars to reimburse their victims, such as lending companies. Over the dozen years I looked at, the average person convicted paid $2 million in restitution for their misdeeds.

More lightning strikes than convictions

It’s impossible to know how common mortgage fraud really is. Some mortgage applications are rechecked in a “post-closing audit.” However, these audits happen within 90 days after the mortgage money is disbursed. Beyond that window, if a loan is paid back on time and without problems, there’s little incentive for a bank or mortgage service provider to recheck an applicant’s information.

What is clear is that while millions of mortgages are written each year, only a tiny fraction of mortgage recipients go to jail for fraud. One way to put this tiny fraction into perspective is to compare it with the National Weather Service estimates of the approximately 270 people hit by lightning yearly. Last year, lightning hit over seven times more people than the federal government convicted of mortgage fraud.

Years ago, I filled in a mortgage application to buy a home. I was consumed with dread wondering if any application mistake would result in my being sent to jail. After looking at the mortgage fraud conviction data, I should have been more worried about being hit by lightning.

This article is republished from The Conversation, a nonprofit, independent news organization bringing you facts and trustworthy analysis to help you make sense of our complex world. It was written by: Jay L. Zagorsky, Boston University

Read more:

- Bandits are losing interest in robbing banks, as some crimes no longer pay

- In defense of cash: why we should bring back the 0 note and other big bills

- Trump’s radical argument that he alone can interpret vague laws fails its first court test in dismissal of Fed governor

Jay L. Zagorsky does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

Reuters US Top

Reuters US Top AlterNet

AlterNet America News

America News Click2Houston

Click2Houston Associated Press US News

Associated Press US News Raw Story

Raw Story Law & Crime

Law & Crime